Freight News:

Old Dominion handily beats Q4 expectations; shares up 8%

Management from less-than-truckload carrier Old Dominion Freight Line maintained the view that volumes will likely turn around by spring during a call with analysts on Wednesday. Before the market opened, the company announced that it had beat quarterly consensus expectations once again.

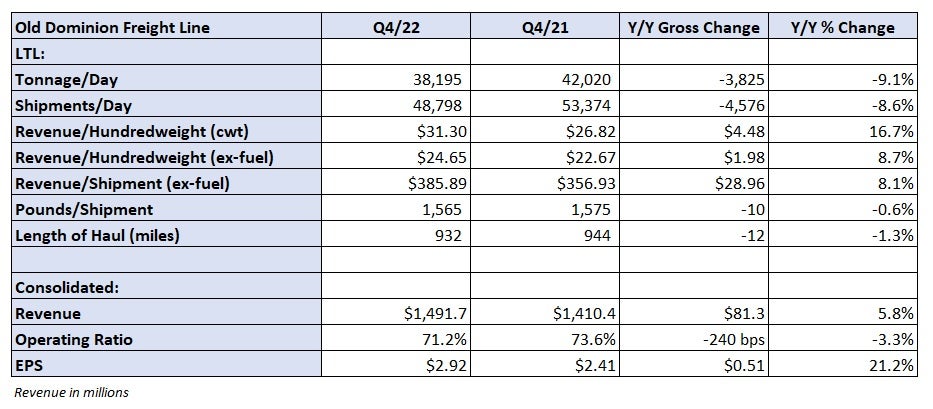

Old Dominion (NASDAQ: ODFL) reported fourth-quarter earnings per share of $2.92, 25 cents ahead of the consensus estimate (according to Seeking Alpha) and 51 cents higher year over year (y/y). The company remains “cautiously optimistic” that volumes are closing in on an inflection.

“We have customers in here every week. Our larger customers, contract customers, come in and it’s business as usual,” Marty Freeman, chief operating officer, stated on the call. “We’re not seeing anything out of the ordinary from an economic circumstance, no major price cutting or anything like that.”

The company announced Tuesday that Freeman would succeed Greg Gantt as president and CEO effective July 1.

“I feel pretty confident that the end is probably near [for] what we’re going through,” Freeman added.

Freeman said he’s not seeing Old Dominion’s customers change service preferences or move freight to regional providers, which has occurred in past downturns.

Revenue in the fourth quarter increased 6% y/y to $1.49 billion. Excluding fuel surcharges, revenue was down roughly 1%. Tonnage per day fell 9% y/y but that decline was more than offset by a 17% increase in revenue per hundredweight, or yield (yield was up 9% excluding fuel). Lower shipments almost entirely led to the tonnage decline.

The lack of a peak shipping season was apparent in Old Dominion’s volumes.

Fourth-quarter tonnage fell 4.4% from the third quarter. The normal sequential step down is just 1.3%. The carrier reported mid- to high-single-digit y/y tonnage declines during October and November, with further acceleration in December, which was down 12%. However, tonnage was down just 8% y/y in January.

Revenue in January was up 4% y/y as a 13% yield increase (up 9% excluding fuel) more than offset the tonnage decline.

Management cautioned that the comp for February (up 18% y/y in February 2022) is formidable but that comps will ease from there. Old Dominion’s tonnage was flat y/y in June, with the declines widening through December.

Old Dominion recorded a 71.2% operating ratio in the quarter, 240 basis points (bps) better y/y. The OR was 210 bps worse than the third quarter but ahead of management’s expectation for a 400-bp decline.

Salaries, wages and benefits were down 290 bps y/y as a percentage of revenue as the company allowed normal attrition to rightsize headcount to lower volumes. The number of average full-time employees was down 3.2% from the third quarter as shipments per day fell 4.6%. Purchased transportation was down 200 bps y/y, which was more than offset by a 260-bp increase in operating supplies (mostly fuel expenses).

Management said the company’s OR normally deteriorates 100 bps from the fourth quarter to the first, but it will likely back up by 200 bps in the 2023 first quarter. The company had a favorable insurance adjustment in the fourth quarter, which presents a 70-bp headwind in the first quarter. Also, it will incur higher depreciation and amortization expense as it ramps equipment buying.

Old Dominion plans to stick to “cost-plus” pricing, reiterating its long-term goal of having revenue per shipment outpace costs per shipment by 100 bps to 150 bps throughout the cycle. Revenue per shipment was 380 bps higher than costs per shipment in the fourth quarter.

“Over the last year … despite the weakness that we’ve seen in the economy, we’ve seen good customer trends,” CFO Adam Satterfield stated. “I think customers have been keeping us in place because one, many are still dealing with [supply chain] challenges … and two, they know that we’re probably closer to things turning and orders picking back up … and they want to make sure that they’ve got capacity that’s available as needed.”

Old Dominion generated $6.26 billion in revenue in 2022, up 19% y/y. That was the second consecutive year the carrier grew revenue by more than $1 billion. Full-year net income was up 33% to $1.38 billion.

Cash flows from operations equaled $1.7 billion in 2022. The company is forecasting total capex of $800 million, with $300 million allocated to new terminals and expansion projects. It will also spend $400 million replacing equipment and $100 million on information technology.

During 2022, Old Dominion recorded $775 million in capex.

Shares of ODFL were up 8% at 12:57 p.m. Wednesday compared to the S&P 500, which was down 0.5%. The better-than-expected report also lifted shares of competitor Saia (NASDAQ: SAIA) by 6.2%. Saia reports fourth-quarter results on Friday.

Year to date, shares of ODFL are up 27% with shares of SAIA up 38%.

More FreightWaves articles by Todd Maiden

- Old Dominion appoints new president and CEO

- Saia’s 6.5% GRI outpaces LTL peers

- Knight-Swift’s Q4 misses, 2023 outlook does not

Import volumes decline in most of the major port markets

videojs.getPlayer('1756640734956317980').ready(function() {

var myPlayer = this;

myPlayer.on("loadedmetadata", function() {

var browser_language, track_language, audioTracks;

browser_language = navigator.language || navigator.userLanguage; // IE <= 10

browser_language = browser_language.substr(0, 2);

audioTracks = myPlayer.audioTracks();

for (var i = 0; i < audioTracks.length; i++) {

track_language = audioTracks[i].language.substr(0, 2);

if (track_language) {

if (track_language === browser_language) {

audioTracks[i].enabled = true;

}

}

}

});

});

The post Old Dominion handily beats Q4 expectations; shares up 8% appeared first on FreightWaves.

Source: freightwaves - Old Dominion handily beats Q4 expectations; shares up 8%

Editor: Todd Maiden