Freight News:

Crude shipping revs up; supertanker rates top $100,000 a day

Spot rates for very large crude carriers (VLCCs) — tankers that carry 2 million barrels of oil — just breached the $100,000-per-day threshold. It could be a taste of things to come. Analysts and investors are increasingly confident that the tanker business is headed into a long, sustained upcycle.

“VLCC rates have surged at the end of the week,” said Clarksons Securities analyst Frode Mørkedal on Friday. Brokerage Fearnleys reported “frenzied activity” in VLCC charter market.

VLCC spot rates averaged $103,900 per day Friday, according to Clarksons. That’s quadruple the five-year average for this time of year. Rates last topped six digits per day in November. They sank to around $38,000 per day in mid-January, near cash breakeven, before rebounding.

“The Middle East is showing the most activity, resulting in a widening earnings gap to the Atlantic Basin,” said Mørkedal.

Middle-East China rates for modern, fuel-efficient VLCCs jumped 20.5% on Friday from the day before, to $102,800 per day. U.S. Gulf-China rates rose 7.5% to $66,500 per day. “We believe rates in the Atlantic will catch up going forward,” he said.

According to Jefferies analyst Omar Nokta, “We count around 50 VLCC fixtures out of the Arabian Gulf this week, which compares to the typical 35 weekly fixtures.” The majority of bookings were for transport to Asia, particularly China, said Nokta.

China demand is ‘incremental catalyst’

VLCCs traditionally earn higher rates than smaller crude tankers and product tankers. More recently, however, VLCCs have at times underperformed Suezmax (1 million-barrel capacity) and Aframax (750,000-barrel capacity) crude tankers, as well as some product tankers.

Sanctions disruptions to Russian exports and European Union imports disproportionately helped rates for smaller tanker classes. Meanwhile, COVID issues in China disproportionately hurt rates for VLCCs, exacerbating normal seasonal weakness.

The market has now shifted. VLCCs “are in the driver’s seat,” said Vortexa analyst Dylan Simpson. “VLCC fundamentals are clearly the most supportive, driving the increase in rates.”

Evercore ISI analyst Jon Chappell told American Shipper, “One hundred thousand dollars a day is not sustainable, but the quick and meaningful move up shows that the market is becoming increasingly tighter.

“A full reopening of China is an incremental catalyst to a market that was already strengthening owing to a global demand recovery and lengthening [voyage distances], even with the biggest importer in the world [China] somewhat on the sidelines for a period of time.

“There are regional ship shortages right now that are making rates go parabolic, but those tend to even out over time,” explained Chappell. “Still, I think higher highs and higher lows are in play for the foreseeable future, barring a global recession or shutting down China again.”

US-China flows show more promise

One of the recent negatives for VLCC rates has been a shift in deployment away from the long-haul U.S.-China route toward the shorter-haul U.S.-Europe route. Tanker demand is measured in ton-miles, volume multiplied by distance. Shorter average trips are negative for demand.

More VLCCs are now heading to China again. Kpler analyst Matthew Wright told American Shipper on Friday, “VLCCs have moved up quite a bit in recent weeks, and a big increase in fixtures from the U.S. to China has played a big part in this. There have been 13 booked so far this month, up from four in February and six in January.”

The number of VLCCs ballasting (sailing empty to a pickup location) to the Atlantic Basin “was in decline from early February to early March, but the firming market is steering more vessels to the area,” said Wright.

“Today, I count 27 ballast VLCCs in the West Indian Ocean heading toward the Cape of Good Hope, up from a recent low of 15 around the middle of February. Based on these trends, we see further upside to rates in the coming weeks.”

Tanker orderbook is historically low

Supply-demand fundamentals appear very positive for tankers in the medium term.

The Russia-Ukraine war fundamentally altered tanker trades, leading to longer voyage distances for both crude and product tankers. These changes look like they’ll stick.

Paula Pinho, the European Commission’s deputy director-general of energy, told the S&P Global CERAWeek conference that Europe’s shift away from Russian energy is “in many ways irreversible.”

Meanwhile, orders for new tankers are historically low. Given construction lead times and the fact that Asian yard slots are already chock full of container ship and LNG carrier orders, there is no possible way to add material crude or product tanker capacity until 2026.

According to Clarksons, the ratio of capacity on order to capacity on the water is now 29% for container ships and 52% for LNG carriers. In sharp contrast, the orderbook-to-fleet ratio for crude tankers is a mere 2.9%, with VLCCs at only 1.9%. The ratio for product tankers is 6%.

More upside for tanker stocks?

The question for stock pickers is whether future rate upside is already baked into tanker share pricing.

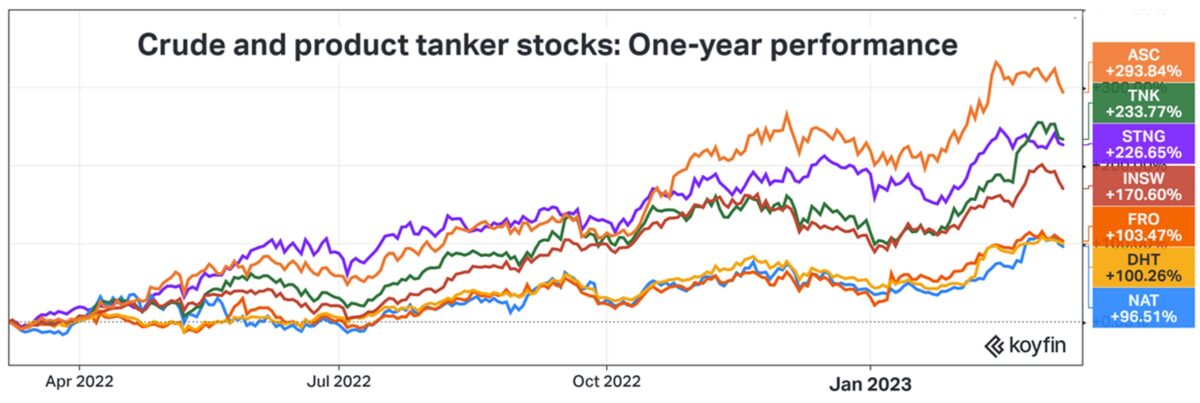

The historically low orderbook is no secret to the investors. Most product tanker and crude tanker stocks have risen by triple digits over the past year.

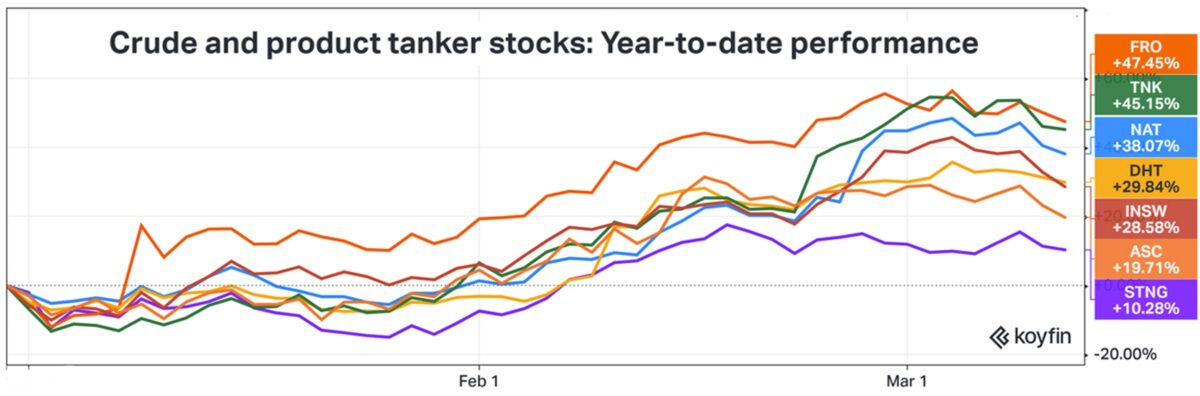

Crude tanker stocks have done particularly well since the start of this year, given the still-developing demand upside from Russian sanctions and China’s reopening, together with the ongoing dearth of new orders on the supply side of the equation.

Whereas one-year gains are more weighted to product-tanker stocks like Scorpio Tankers (NYSE: STNG) and Ardmore Shipping (NYSE: ASC), the year-to-date gains have favored owners with fully or predominantly crude-tanker fleets, like Frontline (NYSE: FRO), Nordic American Tankers (NYSE: NAT) and DHT (NYSE: DHT).

According to Deutsche Bank analysts Amit Mehrotra and Chris Robinson, “While we believe limited fleet growth will help keep rates supported at these strong levels, we believe much of this expectation has already been priced into asset values as well as share prices.”

Mørkedal of Clarksons and Chappell of Evercore sound more optimistic.

“We anticipate that the tanker industry will thrive in the coming years, particularly in 2024 and 2025,” wrote Mørkedal. “Although there are investor concerns that tanker stocks have risen too quickly, we believe the odds of a prolonged upswing cycle are favorable, implying that tanker stocks have significant further upside potential.”

Chappell told American Shipper: “I think we turned the corner a while ago and can now start to contemplate a true cyclical upturn. Given that we are only in the early stages of an upturn, with substantial cash-flow generation and only a sliver of potential dividends distributed at this point, I think tanker stocks are set up very well for the next 12-18 months.”

Click for more articles by Greg Miller

Related articles:

- The rise of crude tanker ‘cannibals’ in wake of Russia-Ukraine war

- One year later: How Ukraine-Russia war reshaped ocean shipping

- Welcome to the dark side: The rise of tanker shipping’s ‘shadow fleet’

- Sanctions effect begins: Crude tankers forced onto longer voyages

- Crude tanker rates down double digits after Russia sanctions debut

- Could Russia sanctions work in practice even if they fail on paper?

- Chaos theory: How tankers thrive amid energy crisis and war

The post Crude shipping revs up; supertanker rates top $100,000 a day appeared first on FreightWaves.

Source: freightwaves - Crude shipping revs up; supertanker rates top $100,000 a day

Editor: Greg Miller