Freight News:

CPG cost pressure begins to ease

CPG cost pressure begins to ease

The biggest economic news on Wednesday was the inflation numbers, with overall CPI and Core CPI coming in at 5.0% and 5.6%, respectively. One component of CPI that is directly related to CPG — food at home prices — was 8.4% higher year over year (y/y) in March and had a seasonally adjusted month-over-month (m/m) decline of 0.3% — the first m/m decline since September 2020.

While moderating consumer inflation is a positive for the CPG industry, moderating inflation in companies’ costs is likely to be more impactful. In an economic cycle, as inflationary pressures intensify, CPG companies’ costs typically increase faster than prices paid by retailers and consumers — those prices are on a lag based on agreements that were put in place when price levels were lower. That dynamic leads to a contraction in CPG margins, which was dramatic in the pandemic period. Most CPG companies’ gross margins remain a few hundred basis points below their pre-pandemic levels.

That CPG margin contraction in response to rising prices should be temporary and, as inflation cools, CPG margins should recover and contracts with retailers catch up. ConAgra’s fiscal third-quarter results last week suggest that a CPG margin recovery may be upon us.

The Hunt’s ketchup maker is seeing a deceleration in its rate of cost growth from 10% for the entirety of its current fiscal year (ending May 31) to 8% in its just-completed fiscal third quarter, to an expectation of a 5.5% increase in its current fiscal quarter (also ending May 31). That deceleration is being driven by a combination of easing supply chain pressure, declines in commodity costs and easing year-ago comparisons.

Breaking down the 8% cost increase in its fiscal Q3, ingredients and materials inflated 10% (two-thirds of its costs), labor cost inflation was in the mid- to high-single digits and there was significant deceleration in transportation and warehousing costs — up only in the low-single digits (see comparison to SONAR data in the section below).

Meanwhile, elasticities have been muted, with changes in sales volume no worse than history would suggest. ConAgra’s retail prices were up a hefty 15% y/y, which resulted in an 8% drop in sales. (The company attributed 100 basis points of that volume drop to lingering supply chain issues.) With most other CPG companies also satisfied with their elasticities, it seems doubtful that companies would cut prices in response to falling commodity costs — thus, CPG margins should recover.

Van contract rates still above reefer rates — at least for now

As CPG companies and other major shippers report earnings, many are certainly reporting moderating logistics costs, as one would expect. However, at the same time, few are not calling out logistics costs as an earnings tailwind despite the extraordinarily loose truckload market. One reason is that freight costs are not usually one of shippers’ largest cost segments — CPG companies often discuss freight costs as being 8%-9% of their cost of sales.

Another reason, as we have discussed frequently, is that large contractual shippers are wary of being too aggressive with contract rates in order to have their loads covered when the market eventually turns.

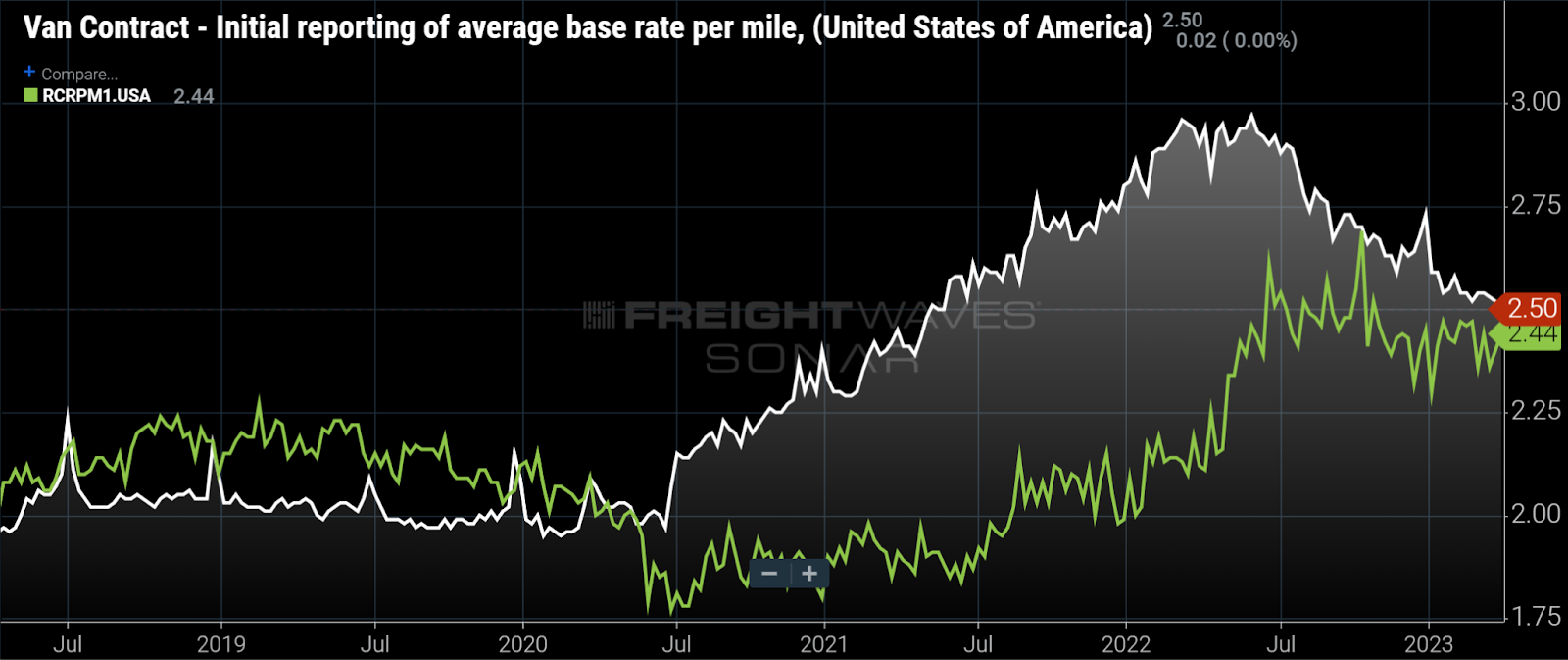

A third reason, which pertains to shippers that utilize both dry van and reefer capacity, may be explained by the above chart, which shows reefer rates holding up better than dry van rates — at least for now.

As I mentioned above, ConAgra said its transportation and warehousing costs had moderated in its just-reported fiscal third quarter — but were still up in the low-single digits y/y. That is easier to reconcile when considering that it likely uses a combination of dry van (where contract rates, excluding fuel, are down double digits, as shown in the white line above), while reefer rates (green line above) are still showing up y/y in our data. It appears that rates for both of those truckload segments have more room to fall, particularly the dry van segment. Normally, dry van rates should be below reefer given the lower equipment and operating costs. That was the case in 2018 and 2019, as shown in the left side of the above chart.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.

The post CPG cost pressure begins to ease appeared first on FreightWaves.

Source: freightwaves - CPG cost pressure begins to ease

Editor: Michael Baudendistel