Freight News:

Convoy shutdown, earnings reports highlight ongoing market weakness

Convoy failure reflects market conditions that continue to benefit shippers

News of Convoy’s failure dominated FreightWaves’ content this week. While the read-throughs are more pronounced for other brokers than for CPGs/retailers (the intended primary audience for this newsletter), there were still numerous takeaways from our content that are important to shippers.

From Craig Fuller’s article, Freight brokerage bubble bursting as freight markets face long winter:

- Freight rates have been very soft all year, and there has been no improvement as bid season (traditionally mid-October through the end of February) gets underway.

- We foresee contract rates dropping further as carriers realize “it’s lower for longer.”

- Spot rates, currently at levels where carriers lose money on many of the miles they run, are unlikely to fall much further.

- FreightWaves has been hearing from sources that a number of other midsize ($50 million-$250 million in revenue) brokers are in financial trouble.

John Kingston’s write-up of Knight-Swift’s earnings suggests that shippers do not have to worry about many loads falling through the routing guide this fall.

- The outlook for TL calls for “muted peak season demand with limited non-contract opportunities.” The company expects spot rates to improve slightly, in line with normal seasonal patterns.

- In its LTL segment, management expects to see a mid-teen year-over-year (y/y) increase in revenue during the fourth quarter as shipments and yield grow by high-single digits.

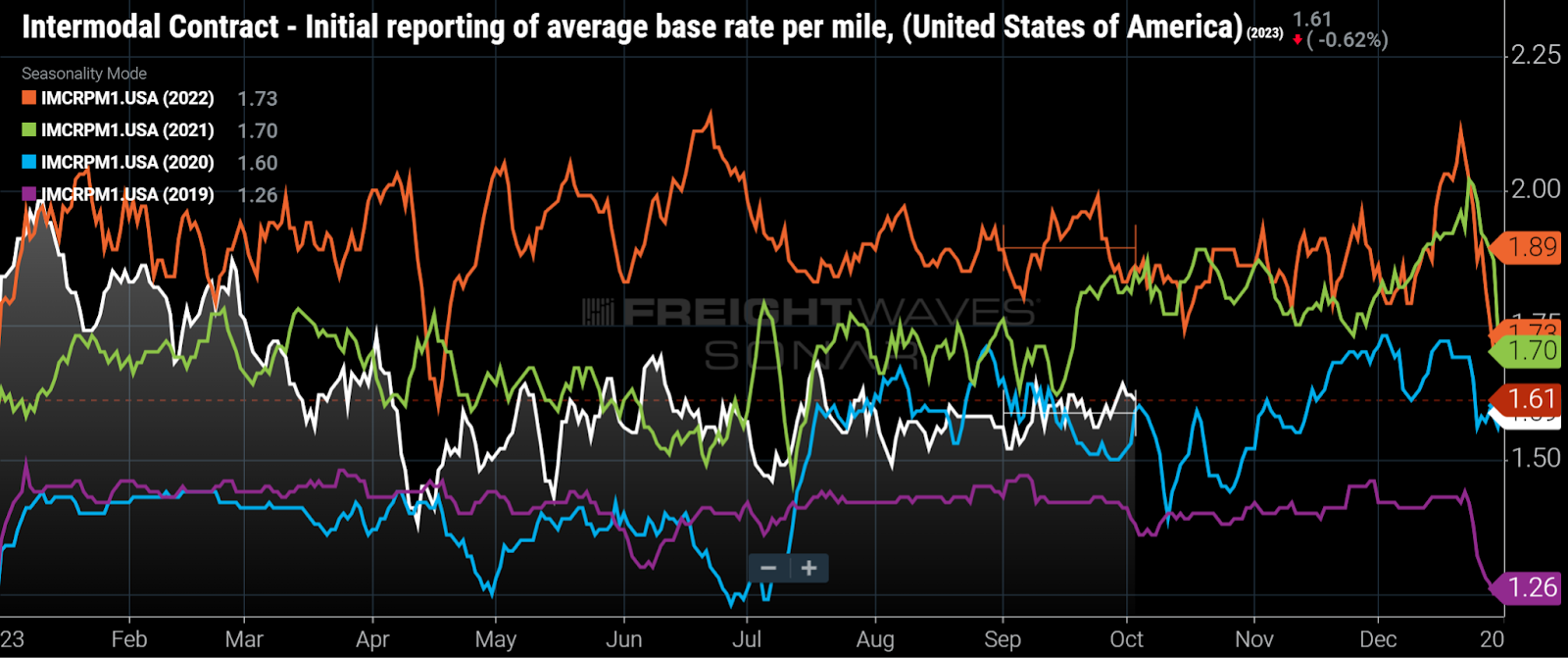

JB Hunt’s earnings highlight continued capacity excesses in domestic intermodal.

- Intermodal revenue per load declined 14% y/y in Q3, excluding fuel.

- The difference between reported trailing equipment at the end of the quarter (117,387 units) and effective trailing equipment usage during the quarter (96,248 units) suggests the equipment was 82% utilized. In that year-ago period it was 96.5%.

Domestic intermodal contract rates, excluding fuel surcharges, were lower by double-digit percentages in the third quarter. (Chart: FreightWaves SONAR)

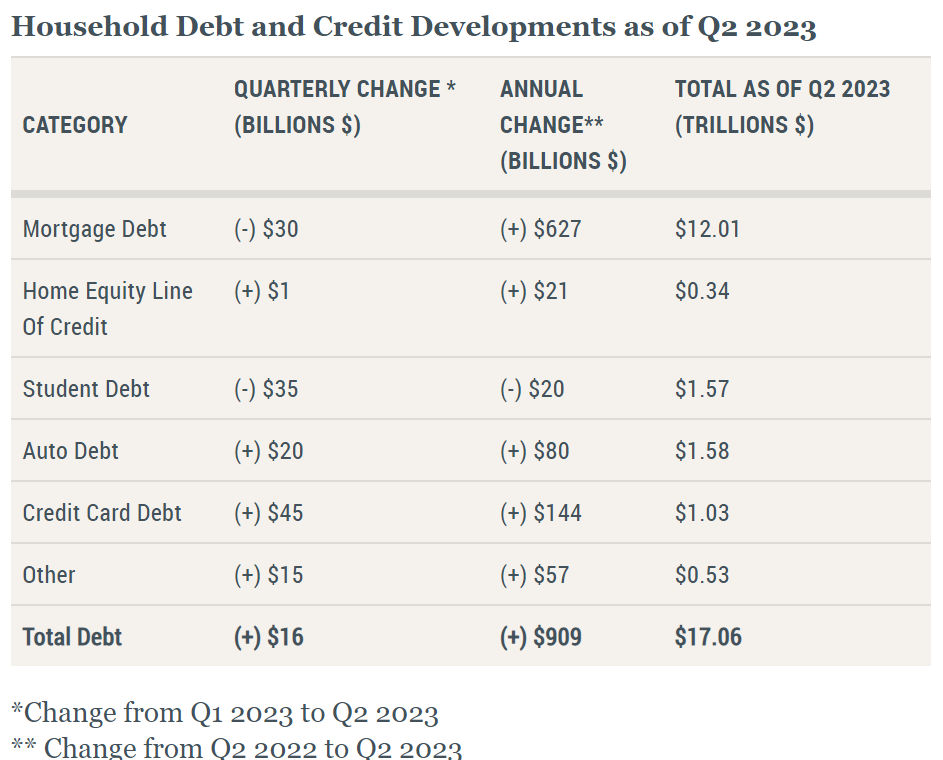

Consumer debt continues to mount

(Chart: NewYorkFed.org)

Credit card debt usually peaks seasonally around the holidays, with the biggest credit card bills landing in January. That is part of why total credit card debt rising above $1 trillion, according to the New York Federal Reserve, is concerning and suggests that the average consumer has little dry powder for holiday spending this year. Consumer debt service payments (not including debt service related to mortgages) represented 5.8% of discretionary income at the end of the second quarter, down from 5.9% at the end of the first quarter, but is otherwise the highest percentage since the Great Recession.

Of course, big-ticket discretionary items, such as furniture and televisions, are likely to be most impacted. Still, consumer pressure is also filtering down into CPG unit sales volume. Last year at this time, many CPG companies were still saying that elasticities were “muted,” or less than what history would suggest given the price increases in everyday items. Now, CPG companies are starting to see elasticities that have risen closer to historical norms.

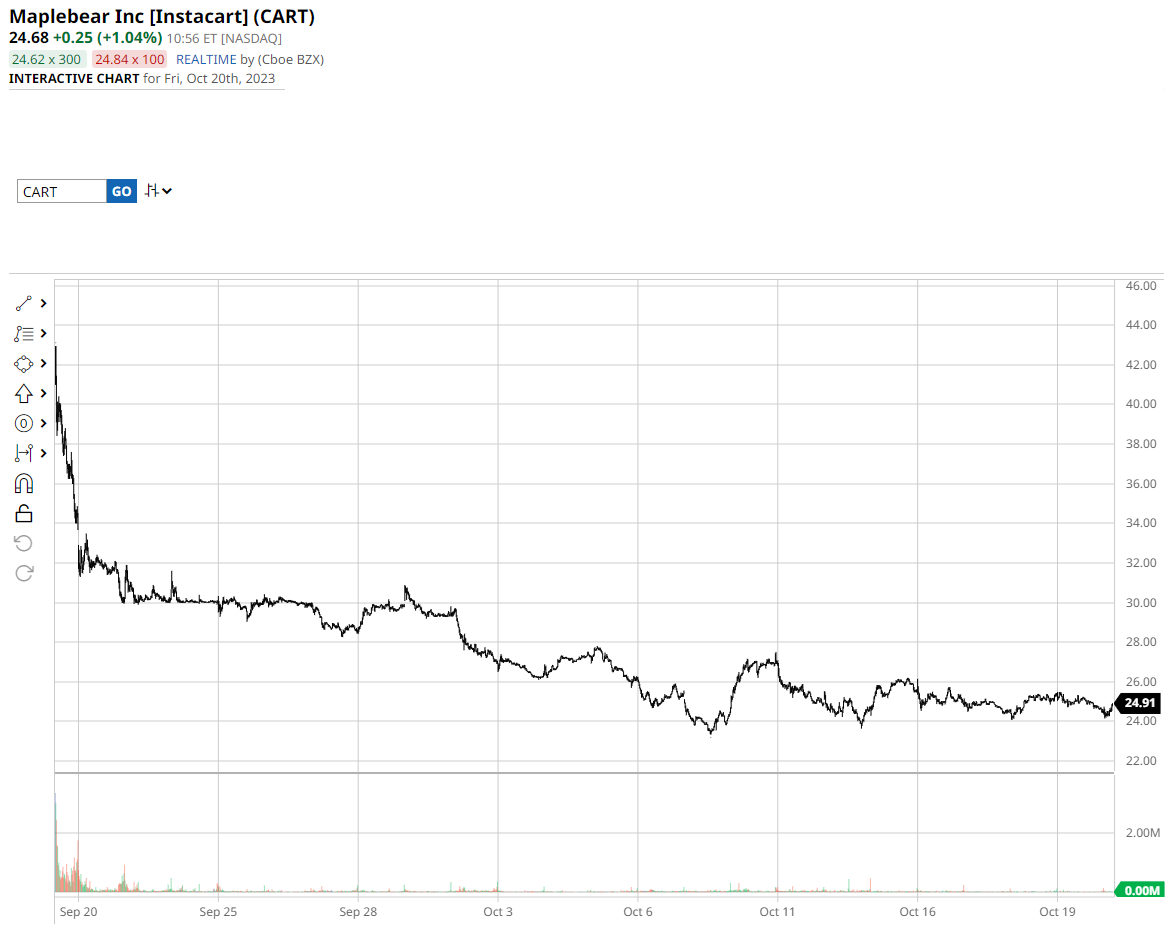

Investors question defensibility of Instacart’s model

(Chart: Barchart.com Inc.)

The Instacart IPO hasn’t helped open the floodgates for new public issuances as some had speculated. Aside from pressures on consumers making them more reluctant to hire an Instacart personal shopper, the technology-based delivery service faces numerous other risks. More retailers could cease using Instacart, particularly as the industry consolidates, and as retailers make investments in their own e-commerce platforms. That risk is highlighted by Whole Foods, which had been a significant Instacart partner in 2018 but ceased using the service in May 2019 following its acquisition by Amazon. The risk of further retail departures is significant with its top three retailers representing 43% of Instacart’s gross transaction value. The volume of orders placed on Instacart has slowed, up just 0.4% y/y in the first half of 2023 from the first half of 2022. Higher-margin advertising revenue is more important than revenue related to fulfilling orders and is likely behind the company’s profitability in 2022 and the first half of 2023, but slowing transaction volume may ultimately be a limiting factor on advertising revenue.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.

The post Convoy shutdown, earnings reports highlight ongoing market weakness appeared first on FreightWaves.

Source: freightwaves - Convoy shutdown, earnings reports highlight ongoing market weakness

Editor: Michael Baudendistel