Freight News:

The Stockout: Consumers start to balk at higher prices

Growing evidence of ‘shopper rebellion’

Elasticities, or the negative change in sales volume in response to rising prices, has been one of the main topics in the CPG industry in the past year. Despite two consecutive years of steeply rising prices, including last year’s CPG price growth of upward of 15% or more in many categories, CPG elasticities have remained below historic norms and have been below most analysts and companies’ internal expectations so far.

However, as consumers become increasingly stretched each month, there is growing evidence that the changes in consumer behavior, which started with big-ticket, discretionary items like televisions and furniture, are extending to everyday items. The Wall Street Journal described this in its “shopper rebellion” article on Monday that adds color to the concerns expressed in last week’s The Stockout article that discussed consumers balking at higher beer prices. In addition to consumers pushing back on rising beverage prices, as Constellation described, the “shopper rebellion” article highlighted Conagra Brands’ 8.4% volume decline in its most recently reported quarter that resulted from its 17% price increase. Known for middle-of-the-range brands like Hunt’s ketchup, that elasticity, which is higher than what many other CPG companies are seeing, highlights the ongoing trend of sales of premium brands holding up better than other price points. Whether sales of CPGs in the premium segments, which cater to higher-income customers who generally do not need to cut back on CPGs since it’s not one of their biggest budget items, continue to defy gravity remains to be seen, but the quote in the WSJ article from a T-shirt maker is well taken — “the consumer’s mind-set has changed.”

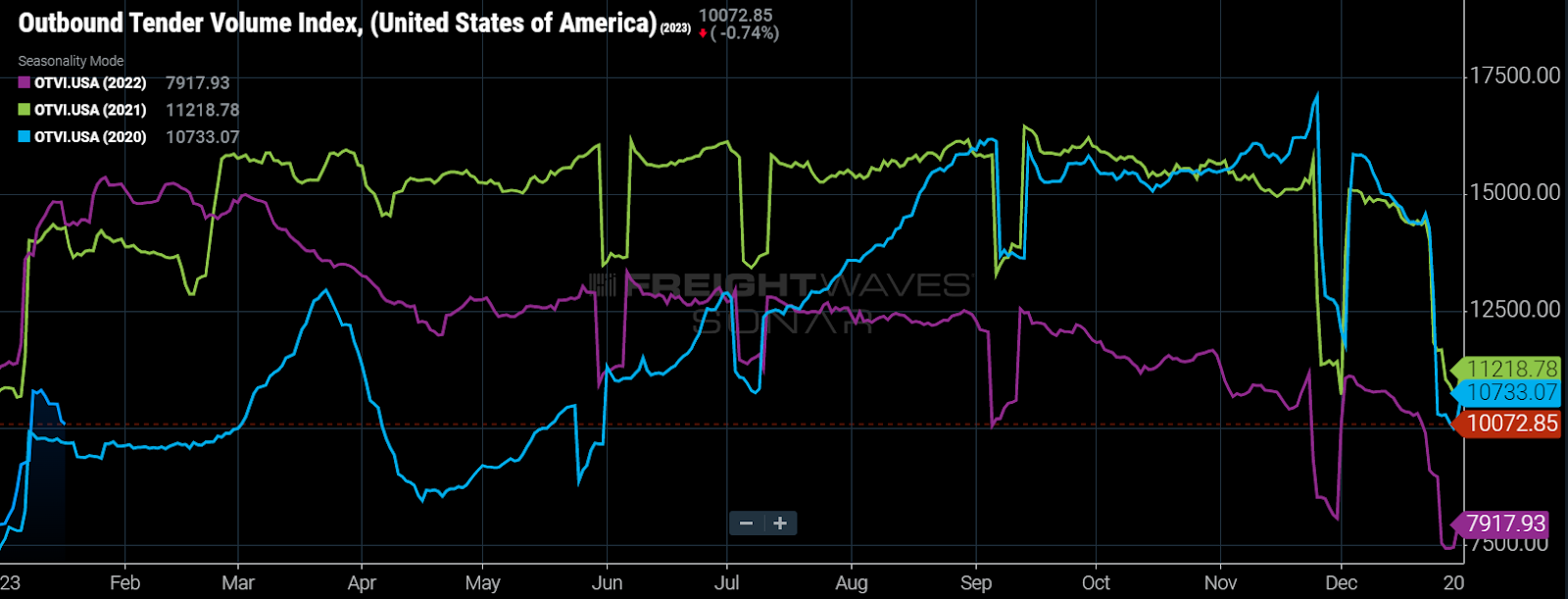

Signs of freight market stabilization

I recommend checking out the article that FreightWaves CEO Craig Fuller published on Monday. Any analysis of the freight markets needs to take seasonality into account and January and February are usually awful for freight demand following plentiful freight demand in November and December. But the last two months of last year were lackluster leading most executives to expect a dreadful start to 2023. Yet truckload tender data and truckload spot rate data have actually defied expectations to the upside.

On the topic of truckload demand, I also recommend reading Zach Strickland’s most recent Chart of the Week article on the influence that import volume has on the truckload market.

Around the web:

Scientist from General Mills gives ideas on whole grain funding

Unilever CEO Alan Jope ‘defends continued presence in Russia’

Kroger-Albertsons merger gets thumbs-down from produce trade groups

Albertsons wraps up chai wide deployment of fresh-food management program

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.

For more information on SONAR or to request a demo, click here.

The post <strong>The Stockout: Consumers start to balk at higher prices</strong> appeared first on FreightWaves.

Source: freightwaves - The Stockout: Consumers start to balk at higher prices

Editor: Michael Baudendistel